![]()

Approximately 70% of all people aged 65 and older will require long-term care at some point in their lives.

801-546-9556

You are one phone call away from learning your financial options for Long Term Care.

“I recommend Utah Senior Planning to everyone. They are wonderful in explaining the process, outlining a plan and following up. I am very impressed with how quickly everything went and how simple they made a very confusing situation.”

— Andrea Brennan, Salt Lake City

“Utah Senior Planning should be commended for their compassion and attention to detail.”

— Bud Carraway, Midvale

UTAH SENIOR PLANNING

Liquidating savings is usually the easiest way to pay for long-term care. However, most families simply do not have enough savings available to pay for their own families, and their parents care as well. If you have a long-term care policy, make sure you know what its exclusions and limitations are. Medicaid and Veteran’s assistance can be obtained with careful planning and guidance, while possibly allowing you to preserve, hard-earned assets for future generations. To give you the expert guidance and assurance of the positive outcome when it comes to applying for financial aid programs as well as preservation of your family’s assets, we partnered with Utah Senior Planning. Utah Senior Planning incorporates an innovative approach to helping seniors prepare for long-term healthcare needs and resolve medical crisis situations. Services provided include:

Liquidating savings is usually the easiest way to pay for long-term care. However, most families simply do not have enough savings available to pay for their own families, and their parents care as well. If you have a long-term care policy, make sure you know what its exclusions and limitations are. Medicaid and Veteran’s assistance can be obtained with careful planning and guidance, while possibly allowing you to preserve, hard-earned assets for future generations. To give you the expert guidance and assurance of the positive outcome when it comes to applying for financial aid programs as well as preservation of your family’s assets, we partnered with Utah Senior Planning. Utah Senior Planning incorporates an innovative approach to helping seniors prepare for long-term healthcare needs and resolve medical crisis situations. Services provided include:

Utah Senior Planning’s vision is to change the way seniors and their families access and qualify for public benefit assistance programs. We’ve been doing just that since 2008 when I founded this company. Since our first applications for Medicaid and V.A. benefits, we’ve vastly improved our process and planning strategies – improvements that only come from experience.

Utah Senior Planning’s vision is to change the way seniors and their families access and qualify for public benefit assistance programs. We’ve been doing just that since 2008 when I founded this company. Since our first applications for Medicaid and V.A. benefits, we’ve vastly improved our process and planning strategies – improvements that only come from experience.

Our experience helps us understand what people in your situation are going through. You may feel overwhelmed by the many moving parts of long-term care, especially how to finance long-term care needs; let us show you how you or your loved one can afford long-term care. We’re always adding to our list of valuable services and we strive to live up to our vision. Our goal is to satisfy our clients and meet all of their potential needs.

Whether it’s mediating disagreements between siblings, years of unfiled tax returns, tracking down missing financial statements or negotiating with nursing facilities, there are few problems that we can’t offer solutions to.

We also work closely with our partner nursing facilities to make sure all parties are coordinating efforts to meet your needs. Let us help you discover how your situation is not nearly as dire as it seems.

All initial meetings and consultations are free and you don’t pay us a dime until we help you put together a plan that everyone agrees with. Take advantage of what we can offer you.

William Sandberg

President Utah Senior Planning

Your Satisfaction is our Top Priority

Utah Senior Planning is an independent insurance brokerage, meaning that our top priority is finding the right Medicare insurance for you – not selling the plan with the highest commissions. Our licensed agents are available to meet and discuss individual needs for medical and prescription coverage. By researching all of the available Medicare plans in Utah, we’ll find the plan that is tailored to meet your needs.

Yearly Reviews

Every annual enrollment period, which usually begins in October and ends in December, we’ll review your needs and current coverage with you and let you know of any upcoming changes in your plan for the following year. We’ll also make recommendations if there are any plans available that would be a better fit for your needs.

Plan Types

Our agents are licensed to offer Medicare Supplements, Medicare Advantage Plans (HMOs) and Prescription Drug Plans. We’ll review the pros and cons of each plan type and listen carefully to your feedback to make the best recommendation for you.

Locally Owned, Community Oriented

Utah Senior Planning has been serving Utah’s seniors since 2005. We are locally owned and operated and we strive to help members of our community find the right coverage for their needs. Our objective information and superior service can help you minimize your healthcare expenses.

The V.A. Aid and Attendance Pension is available to help veterans and their spouses obtain financial aid to pay for long-term care costs. Expenses for home healthcare, assisted living facilities or skilled nursing facilities are among the many expenses that qualify you to receive a pension from the V.A.

2021 Maximum Pension Rates*

Single Veteran $1,759 per month or $21,108 per year

Married Veteran $2,085 per month or $25,020 per year

Widowed Spouse of a Veteran $1,130 per month or $13,560 per year

Veteran married to a Veteran $2,761 per month or $33,132 per year

Each Additional Dependent $180 per month or $2,160 per year

*Rates listed are maximum possible benefit payments. Not all veterans will qualify to receive the maximum amounts.

To qualify for the Aid & Attendance benefit, veterans must meet the following conditions:

1. Veteran must have served at least 90 days of active military service with at least one day being during a wartime period.

Official periods of war include:

World War II, 12/07/1941 – 12/31/1946

Korean Conflict, 06/27/1950 – 01/31/1955

Vietnam War, 08/05/1964 – 05/07/1975 (02/28/1961 if served in Vietnam)

Persian Gulf War, 08/02/1990 – TBD

2. Veteran must have received a military discharge other than dishonorable. Military discharges include, from highest to lowest: honorable, general, other than honorable, bad conduct, and dishonorable.

3. Veteran must be in need of the daily aid and attendance of another person in order to avoid the everyday hazards of his or her environment. Includes help with prescription management, bathing, toileting, dressing, getting gin and out of bed and other activities of daily living.

Purpose

The New Choices Waiver is designed to transition eligible patients from a skilled nursing facility to an assisted living facility while maintaining Medicaid eligibility and assistance.

Skilled Nursing vs. Assisted Living

A skilled nursing facility offers a high level of care and serves people with extensive and demanding care needs. Most long-term care residents in a skilled nursing facility will have a shared room. An assisted living facility is a care facility that offers more basic care giving services. Assisted living facility residents usually have a private room and are allowed more independence than skilled nursing. Patients must be physically and financially eligible to qualify for the New Choices Waiver.

Eligibility Requirements

- Must meet 2 of 3 assisted living level of care criteria

- Financially eligible for long-term care Medicaid

- The primary health condition must not be attributable to a mental illness

Individuals must also meet at least one of the following criteria:

– Residency in a skilled nursing facility for 90+ days, with at least 30 days covered by Medicaid

– Residing in a Medicaid licensed assisted living facility for at least five months

Assisted Living Care Criteria

- Unable to complete activities of daily living without substantial physical assistance above and beyond verbal prompting or supervising.

- Physician determination reflects that the person has a high enough level of disorientation to person, place or time that they require nursing facility care.

- Care needs or medical condition require more services and support that can be delivered in a less structured setting than a nursing facility.

Using Medicaid Policy to Your Advantage

The Long-Term Care Medicaid program is confusing and difficult to get approved for, even if you’re already eligible.

Making matters worse, there are many misconceptions about how to qualify for and apply for Medicaid assistance.

We can help you understand the complicated process of getting the help you or your loved one needs to pay for long-term care in a skilled nursing facility.

One of the most common misconceptions about Long-Term Care Medicaid policy is that if you have any assets at all, you don’t qualify for assistance. This simply isn’t true.

We can answer all the common questions that seniors have about Medicaid:

- Do I need to spend down all my assets to qualify for Medicaid?

- Will my spouse living at home have enough money to pay for living expenses?

- How long does it take to get approved for long-term Medicaid coverage?

- Are my Veteran benefits compliant with Medicaid?

- What medical service does Medicaid cover?

- If I accept Medicaid assistance, can the state seize my house from my spouse or loved one after I die?

- Are my children responsible for my medical bills?

We guarantee to get you or your loved one eligible and approved for Medicaid

Utah Senior Planning incorporates an innovative approach to helping people become eligible for Medicaid, including financial and legal planning. We specialize in Medicaid preplanning, asset preservation and crisis management. We can help you if you’re already in a nursing home and need help qualifying or if you’re anticipating a future need. Additionally, we will be your advocate with Medicaid and will handle all correspondence related to your application. Contact us for a free consultation.

A Worthwhile Experience

There are many emotional as well as financial benefits with a pre-planned and pre-paid funeral.

A funeral is one of the most personal and emotional events your family will ever share.

A family discussion of funeral planning, although sensitive, can be a very worthwhile experience for you and the ones you love.

Emotional and Financial Benefits

We believe pre-planning is a smart decision for everyone regardless of age.

Some of the benefits of advanced funeral planning include:

- Alleviating the difficulties of decision making in a time of grief

- Guaranteed prices – the cost of your funeral won’t be affected by inflation

- Surviving family members are not left with the expense

- Minimized confusion and anxiety for your surviving family members

- Prevention of emotional over-spending

Experienced Agents

Utah Senior Planning retains family counselors with more than 20 years of experience in final expense planning who are available to answer any questions you may have about making final arrangements. By working with a trained and licensed agent, you’ll gain an understanding of the many decision that need to be made surrounding your or a loved one’s passing.

Get the Most out of Your Money

Now, more than ever, Americans should take steps to maximize the benefits of tax planning strategies.

Proper tax planning can reduce eventual estate taxes, augment the amount of funds you will have available for retirement and assist you in managing cash flow to help meet your financial objectives.

Nearly all financial decision have tax ramifications. Tax liabilities associated with income, estate, gift and various state, excise and sales taxes can take a real toll on your wealth.

Our team of experienced professionals can help coordinate the various aspects of your financial plan to maximize tax-efficient strategies in line with pursuing your overall financial goals.

Proper tax planning can achieve the following goals:

- Maximize the amount of money you will have for retirement

- Lower this year’s tax

- Defer this year’s tax to future years

- Reduce your tax in future years

- Maximize the tax savings from allowable deductions

- Take advantage of available tax credits

- Maximize the amount of wealth that stays in your family

- Minimize capital gains tax

- Avoid penalties for underpayment of estimated taxes

- Free up cash for investment, business or personal needs

- Transfer assets to loved ones in the most tax efficient manner

- Manage your cash flow by projecting when tax payments will be required

- Minimize estate taxes to leave the most money possible to beneficiaries rather than the government

Be Prepared

As millions of baby boomers head into retirement, many discover that they were not as well prepared as they had thought.

As individuals prepare for retirement, it’s important to be aware of some of the more common retirement planning pitfalls.

We understand the unique needs and challenges faced by seniors who are retired or are about to retire.

It’s important to understand how your retirement income should be structured, how long your income will last and which sources of income you should tap into first to minimize taxes and maximize income potential.

It’s Never Too Early To Plan

Whether you are in the accumulation phase or have already retired, a sound strategy is critical. Through comprehensive planning, we can help you prioritize your goals, develop a strategy to protect and grow your retirement assets and minimize your tax liability – now and during retirement. One of the most common mistakes we see people make in planning their retirement is a failure to plan for the potential expense of long-term care; this is another important facet of retirement planning that we can help you plan for.

- As part of our planning, we evaluate the variables in your retirement plan to ensure that you are able to:

- Meet your retirement income needs, desires and expenses

- Maintain your lifestyle choices and priorities

- Fund your long-term goals and aspirations, whether they be travel, long-term healthcare, estate planning, charitable giving or any other goals

Retirement Tools

- 401(k) / 403 (b) Retirement Plans

- Traditional and Roth IRAs

- Guaranteed Issue Annuities

- Social Security Election Planning

- Long-term Care Insurance

- 401(k) / IRA Rollovers

- Annuities

Planning your estate will help you organize financial record and prevent potential problems in the future

Would your family know where to find your financial records, titles and insurance policies if something happened to you?

Planning for your estate now will help you organize your records, locate titles and beneficiary designations, and find and correct errors. Most people don’t give much thought to the wording they put on titles and beneficiary designations.

You may have good intentions, but an innocent error can create all kinds of problems for your family at your disability and/or death. Beneficiary designations are often out-of-date or otherwise invalid.

Naming the wrong beneficiary on your tax-deferred plan, such as IRA or 401(k) accounts, can lead to devastating tax consequences. It’s much better to take the time to do this correctly now than for your family to pay an attorney to try to fix problems later.

Estate planning does not have to be expensive

If you don’t think you can afford a complex estate plan now, start with what you can afford. For a young family or single adult, that may mean a will, term life insurance, and powers of attorney to manage your assets and health care decision in case of your incapacitation. Then, let your planning develop and expand as your needs change and your financial situation improves. Don’t try to do this yourself to save money. An experienced attorney will be able to provide critical guidance and peace of mind that your documents are prepared properly.

The best time to plan your estate is now

Nobody really likes to think about their own mortality or the possibility of being unable to make decisions for themselves. This is exactly why so many families are caught off-guard and unprepared when incapacity or death does strike. Don’t wait. You can put something in place now and change it later, which is exactly the way estate planning should be done.

The best benefit is peace of mind

Knowing you have a properly prepared plan in place – one that contains your instructions and will protect your family – will give you and your family peace of mind. This is one of the most thoughtful and considerate things you can do for yourself and for those you love.

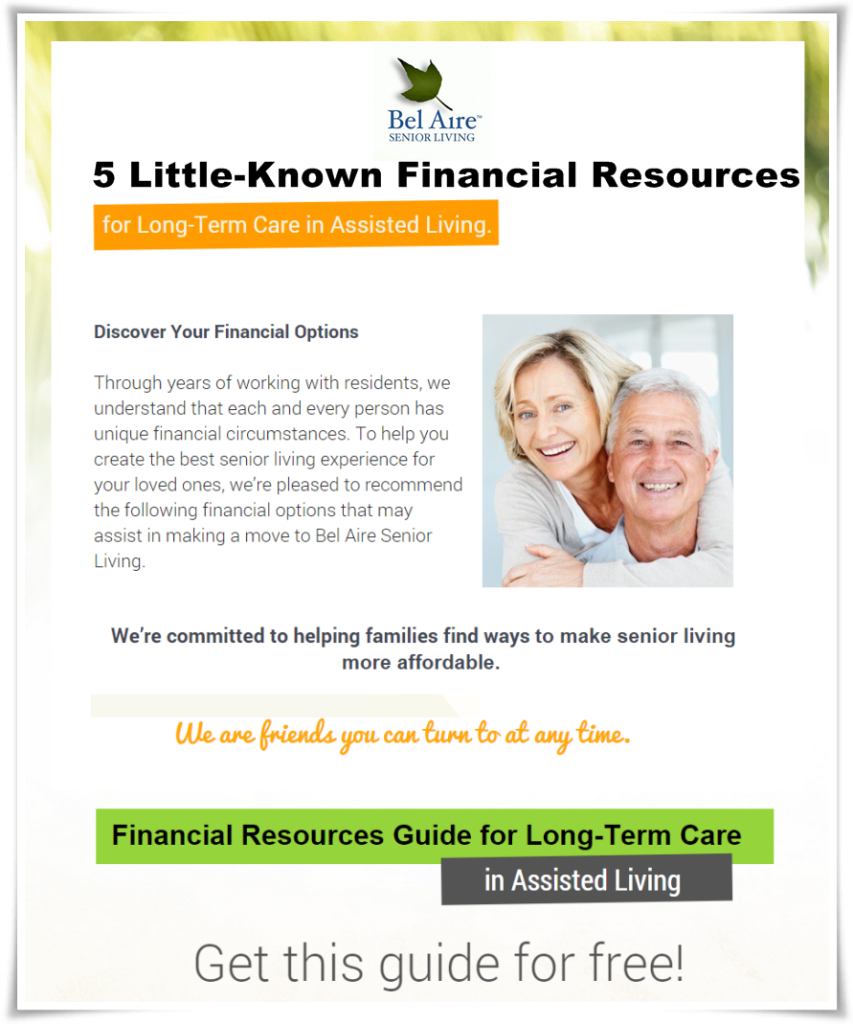

FREE DOWNLOAD

5 Little-Known Financial Resources for Long-Term Care

Since Medicare doesn’t pay for long-term care, how can you afford it?

Long Term Care includes, nursing homes, hospice care, rehabilitation care and Assisted Living Centers. However, Medicare doesn’t pay for long-term care. (Source www.medicare.gov). Some financial options available to you are:

- Paying from your life’s savings or your family’s life savings

- Veteran’s Long-Term Care Benefits

- Paying from a long term care insurance policy

- Applying for Medicaid assistance

Download the FREE GUIDE below to learn more.

“Without the help of Utah Senior Planning, we would still be struggling with the paperwork for Medicaid…It is such a relief to have this team, that knows exactly what to do. Everyone there was such a help and is still working with us.”

Third-Party Legal Services Available

- Powers of Attorney

- Wills/Trusts

- Social Security Disability

- Guardian/ Conservator

- Wealth transfer strategies

- Caregiver Agreements

- (Mobile) Notary Service

“Even if there is no “magic” solution that will work perfectly for every person we are grateful that we partnered with Utah Senior Planning. With careful planning and guidance, we gained access to financial resources for long-term care services. I recommend you give them a call even if you currently don’t think you could qualify!”

Address

1330 Flint Meadow Drive

Kaysville, UT 84037

Even though they are located in Kaysville, you can schedule an appointment to meet with them directly in our Bel Aire Facility in American Fork.

Phone

1-801-546-9556

Fax

1-866-478-2710